Chairman Paul and members of the subcommittee, I am deeply honored to appear before you to testify on the topic of fractional-reserve banking. Thank you for your invitation and attention.

In the short time I have, I will give a brief description of fractional reserve-banking, identify the problems it presents in the current institutional setting, and suggest a potential solution.

A bank is simply a business firm that issues claims to a fixed sum of money in receipt for a deposit of cash. These claims are payable on demand and without cost to the depositor. In today’s world these claims may take the form of checkable deposits, so called because they can be transferred to a third party by writing out a check payable to the party named on the check. They may also take the form of so-called “savings” deposits with limited or no checking privileges and that require withdrawal in person at one of the bank’s branches or at an ATM. In the United States, the cash for which the claim is redeemable are Federal Reserve notes — the “dollar bills” that we are all familiar with.

Fractional-reserve banking occurs when the bank lends or invests some of its depositors’ funds and retains only a fraction of the deposits in cash. This cash is the bank’s reserves. Hence the name fractional-reserve banking. All commercial banks and thrift institutions in the United States today engage in fractional–reserve banking.

Let me illustrate how fractional-reserve banking works with a simple example. Assume that a bank with deposits of $1 million makes $900,000 of loans and investments. If we ignore for simplicity the capital paid in by its owners, this bank is holding a cash reserve of 10 percent against its deposit liabilities. The deposits constitute the bank’s liabilities because the bank is contractually obligated to redeem them on demand. The assets of the bank are its reserves, loans, and investments. Bank reserves consist of the dollar bills in its vaults and ATMs and the bank’s deposits at the Federal Reserve, which can be cashed on demand for dollar bills printed by the Bureau of Engraving and Printing at the order of the Fed. The bank’s loans and securities are noncash assets that are titles to sums of cash payable only in the near or distant future. These assets include short-term business loans, credit-card loans, mortgage loans, and the securities issued by the US Treasury and foreign financial authorities.

Now the key to understanding the nature of fractional-reserve banking and the problems it creates is to recognize that a bank deposit is not itself money. It is rather a “money substitute,” that is, a claim to standard money — dollar bills — universally regarded as perfectly secure.

Bank deposits transferred by check or debit card will be routinely paid and received in exchange in lieu of money only as long as the public does not have the slightest doubt that the bank that creates these deposits is able and willing to redeem them without delay or expense.

Under these circumstances, bank deposits are eagerly accepted and held by businesses and households and regarded as indistinguishable from cash itself. They are therefore properly included as part of the money supply, that is, the total supply of dollars in the economy.

The very nature of fractional-reserve banking, however, presents an immediate problem. On the one hand, all of a bank’s deposit liabilities mature on a daily basis, because it has promised to cash them in on demand. On the other, only a small fraction of its assets is available at any given moment to meet these liabilities. For example, during normal times, US banks effectively hold much less than 10 percent of deposits in cash reserves. The rest of a bank’s liabilities will only mature after a number of months, years, or, in the case of mortgage loans, even decades. In the jargon of economics, fractional-reserve banking always involves “term-structure risk,” which arises from the mismatching of the maturity profile of its liabilities with that of its assets.

In layman’s terms, banks “borrow short and lend long.” The problem is revealed when demands for withdrawal of deposits exceeds a bank’s existing cash reserves. The bank is then compelled to hastily sell off some of its longer-term assets, many of which are not readily saleable. It will thus incur big losses. This will cause a panic among the rest of its depositors who will scramble to withdraw their deposits before they become worthless. A classic bank run will ensue. At this point the value of the bank’s remaining assets will no longer be sufficient to pay off all its fixed-dollar deposit liabilities and the bank will fail.

A fractional-reserve bank, therefore, can only remain solvent for as long as public confidence exists that its deposits really are riskless claims on cash. If for any reason — real or imagined — the faintest suspicion arises among its clients that a bank’s deposits are no longer payable on demand, the bank’s reputation as an issuer of money substitutes vanishes overnight. The bank’s brand of money substitutes is then instantly extinguished and people rush to withdraw their deposits in cash — cash that no fractional-reserve bank can provide on demand in sufficient quantity. Thus the threat of brand extinction and insolvency is always looming over fractional-reserve banks.

In other words, a fractional-reserve bank must develop what Ludwig von Mises called a “special kind of good will” in order to create a clientele who treats their deposits as money substitutes. On a free market this kind of good will is very difficult and costly to acquire and maintain. This reputational asset is what induces a bank’s clients to forebear from immediately cashing in their deposit claims and driving the bank into instant insolvency. Of course to remain profitable the bank must also build up conventional business good will, which depends upon convenient geographical location, outstanding customer service, attractive facilities, the reputation of its management team and so on. But unlike the common form of good will essential to all successful business ventures, the good will that is necessary for a particular bank’s brand of deposits to circulate as money substitutes is indivisible. In almost all other industries, customer good will can be gained or lost in marginal units and does not typically vanish all at once, destroying its product brand and plunging the firm into immediate insolvency.

Ludwig von Mises described the loss of confidence in a bank’s solvency and the related phenomenon of brand extinction in the following terms:

The confidence which a bank and the money-substitutes it has issued enjoy is indivisible. It is either present with all its clients or it vanishes entirely. If some of the clients lose confidence the rest of them lose it too.… One must not forget that every bank issuing fiduciary media is in a rather precarious position. Its most valuable asset is its reputation. It must go bankrupt as soon as doubts arise concerning its perfect trustworthiness and solvency. [1]

The issuing of deposits not fully backed by cash is therefore always a precarious business on the free market. The slightest doubt about the bank’s solvency among even some of its clients will instantly destroy the character of its deposits as money substitutes. Furthermore, the loss of confidence that causes this phenomenon of “brand extinction” is the cause and not the result of a run on the bank and cannot be deterred by a high ratio of reserves to deposits. For under fractional-reserve banking, by definition, reserves are always insufficient to pay off all the demand liabilities that the bank has incurred. In fact the level of cash reserves is not directly relevant to the stability of a bank. It is simply one of several factors that a bank’s clients take into account in forming their subjective judgment concerning whether a bank’s brand of notes and deposits are or are not money substitutes. For example in the 19th century the ratio of gold reserves to notes and deposits of the Bank of England are reported to have been as low as 3 percent, yet it was generally regarded as one of the most stable financial institutions in the world.

The peculiar and overriding importance of public confidence in sustaining fractional-reserve banking was particularly emphasized by Murray N. Rothbard:

But in what sense is a bank “sound” when one whisper of doom, one faltering of public confidence, should quickly bring the bank down? In what other industry does a mere rumor or hint of doubt bring down a mighty and seemingly solid firm? What is it about banking that public confidence should play such a decisive and overwhelmingly important role? The answer lies in the nature of our banking system, in the fact that both commercial banks and thrift banks have been systematically engaging in fractional-reserve banking: that is, they have far less cash on hand than there are demand claims to cash outstanding.[2]

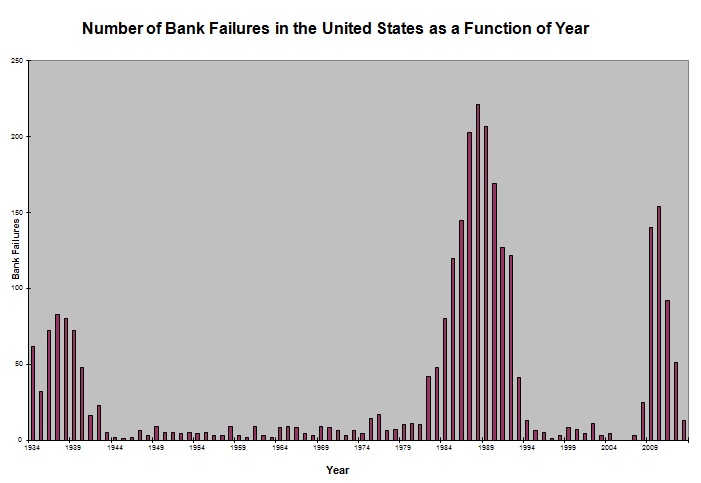

Rothbard’s point about the extreme fragility of public confidence in issuers of fractionally-backed money substitutes is well illustrated by the stunning collapse of Washington Mutual (WaMu) in September 2008, the largest bank failure in United States history. WaMu had been in existence for 119 years and was the sixth-largest bank in the United States with assets of $307 billion. It had branches throughout the country and billed itself as the Walmart of banking. It was one of the top performers on Wall Street until shortly before its failure. Its depositors clearly had enormous confidence in its solidity, especially given that its deposits were insured by the federal government reinforced by the existence of the Fed’s “too-big-to-fail” policy. And yet, almost overnight the special good will that gave its deposits the quality of money substitutes vanished as panic-stricken depositors rushed to withdraw their funds. The unlikely event that triggered the sudden loss of confidence and subsequent brand extinction was the failure of Lehman Brothers, a venerable investment house. A week after Lehman failed, mighty WaMu was no more.

The highly publicized Lehman Brothers failure had shaken public confidence in the solvency not only of WaMu but of the entire banking system. Had the Fed and Treasury not acted aggressively to bail out the largest banks in the fall of 2008, there is no doubt that the entire system would have collapsed in short order. Indeed on a single day in December, the combined emergency lending by the Fed and the US Treasury had risen to a peak of $1.2 trillion. The recipients of these billions included some of the most trusted and reputable brand names in banking: Citibank, Bank of America, Morgan Stanley, as well as European banks like the Royal Bank of Scotland and UBS AG. Without this unprecedented bailout, these discredited brand names would have been relegated to the dustbin of business history

The ever-present threat of insolvency is a relatively minor problem with fractional-reserve banks, however. Its effects are restricted to the bank’s stockholders, creditors, and depositors who voluntarily assume the peculiar risks involved in this business.

The major problems with fractional-reserve banking are its harmful effects on the overall economy caused by the related phenomena of inflation and business cycles.

First, fractional-reserve banking is inherently inflationary. When a bank lends out its clients’ deposits, it inevitably expands the money supply. For example, when people deposit an additional $100,000 of cash in the bank, depositors now have an additional $100,000 in their checking accounts while the bank accumulates an additional $100,000 of cash (dollar bills) in its vaults. The total money supply, which includes both dollar bills in circulation among the public and dollar balances in bank deposits, has not changed. The depositors have reduced the amount of cash in circulation by $100,000, which is now stored in the bank’s vaults, but they have increased the total deposit balance that they may draw on by check or debit card by the exact same amount. Suppose now the loan officers of the bank lend out $90,000 of this added cash to businesses and consumers and maintain the remaining $10,000 on reserve against the $100,000 of new deposits. These loans increase the money supply by $90,000 because, while the original depositors have the extra $100,000 still available on deposit, the borrowers now have an extra $90,000 of the cash they did not have before.

The expansion of the money supply does not stop here however, for when the borrowers spend the borrowed cash to buy goods or to pay wages, the recipients of these dollars redeposit some or all of these dollars in their own banks, which in turn lend out a proportion of these new deposits. Through this process, bank-deposit dollars are created and multiplied far beyond the amount of the initial cash deposits. (Given the institutional conditions in the United States today, each dollar of currency deposited in a bank can increase the US money supply by a maximum of $10.00.) As the additional deposit dollars are spent, prices in the economy progressively rise, and the inevitable result is inflation, with all its associated deleterious effects on the economy.

Fractional-reserve banking inflicts another great harm on the economy. In order to induce businesses and consumers to borrow the additional dollars created, banks must reduce interest rates below the market-equilibrium level determined by the amount of voluntary savings in the economy. Businesses are misled by the artificially low interest rates into borrowing to expand their facilities or undertake new long-term investment projects of various kinds. But the prospective profitability of these undertakings depends on expectations that bank credit will remain cheap more or less indefinitely. Consumers, too, are deceived by the lower interest rates and rush to purchase larger residences or vacation homes. They take out second mortgages on their homes to buy big-ticket luxury items. A false economic boom begins that is doomed to turn into a bust as soon as interest rates begin to rise again.

As the inflationary boom progresses and prices rise, the demand for credit becomes more intense at the same time that more cash is withdrawn from bank deposits to finance the purchase of everyday goods. The banks react to these developments by sharply raising interest rates and contracting loans and deposits, causing a decline in the money supply. Indeed the money supply may very well collapse, as it did in the early 1930s, because the public loses confidence in the banks and demands it deposits back in cash. In this case, a series of bank runs ensue that pushes many fractional-reserve banks into insolvency and instantly extinguishes their money substitutes, which had previously circulated as part of the money supply. Recession and deflation results and the binge of bad investments and overconsumption is starkly revealed in the abandoned construction projects, empty commercial buildings, and foreclosed homes that litter the economic landscape. At the end of the recession it turns out that almost all households and business firms are made poorer by fractional-reserve bank-credit expansion, even those who may have initially gained from the inflation.

Inflation and the boom-bust cycles generated by fractional-reserve banking are enormously intensified by Federal Reserve and US-government interference with the banking industry. Indeed, this interference is justified by economists and policymaker precisely because of the instability of the fractional-reserve system. The most dangerous forms of such interference are the power of the Federal Reserve to create bank reserves out of thin air via open market operations, its use of these phony reserves to bail out failing banks in its role as a lender of last resort, and federal insurance of bank deposits. In the presence of such polices, the deposits of all banks are perceived and trusted by the public as one homogeneous brand of money substitute fully guaranteed by the Federal government and backed up by the Fed’s power to print up bank reserves at will and bail out insolvent banks. Under the current monetary regime, there is thus absolutely no check on the natural propensity of fractional-reserve banks to mismatch the maturity profiles of their assets and liabilities, to expand credit and deposits, and to artificially depress interest rates. Without fundamental change in the US monetary system, the growth of bubbles in various sectors of the economy and subsequent financial crises will continue unabated.

The solution is to treat banking as any other business and permit it to operate on the free market — a market completely free of government guarantees of bank deposits and of the possibility of Fed bailouts. In order to achieve the latter, federal deposit insurance must be phased out and the Fed would have to be permanently and credibly deprived of its legal power to create bank reserves out of nothing. The best way to do this is to establish a genuine gold standard in which gold coins would circulate as cash and serve as bank reserves; at the same time the Fed must be stripped of its authority to issue notes and conduct open-market operations. Also, banks would once again be legally enabled to issue their own brands of notes, as they were in the 19th and early 20th century.

Once this mighty rollback of government intervention in banking is accomplished, each fractional-reserve bank would be rigidly constrained by public confidence when issuing money substitutes. One false step — one questionable loan, one imprudent emission of unbacked notes and deposits — would cause instant brand extinction of its money substitutes, a bank run, and insolvency.

In fact on the banking market as I have described it, I foresee the ever-present threat of insolvency compelling banks to refrain from further lending of their deposits payable on demand. This means that if a bank wished to make loans of shorter or longer maturity, they would do so by issuing credit instruments whose maturities matched the loans. Thus for short-term business lending they would issue certificates of deposits with maturities of three or six months. To finance car loans they might issue three-year or four-year short bonds. Mortgage lending would be financed by five- or ten-year bonds. Without government institutions like Fannie Mae and Freddie Mac — backed by the Fed’s money-creating power — implicitly guaranteeing mortgages, mortgage loans would probably be transformed into shorter five- or ten-year balloon loans, as they were until the 1930s. The bank may retain an option to roll over a mortgage loan when it comes due pending a reevaluation of the mortgagor’s current financial situation and recent credit history as well as the general economic environment. In short, on a free market, fractional-reserve banking with all its inherent problems would slowly wither away.

Notes

[1] Ludwig von Mises, Human Action: A Treatise on Economics. Scholar’s Ed. (Auburn, AL: Ludwig von Mises Institute, 1998), pp. 442, 444.

[2] Murray N. Rothbard, Making Economic Sense, 2nd ed. (Auburn, AL: Ludwig von Mises Institute, 2006), p. 326.

Joseph Salerno is academic vice president of the Mises Institute, professor of economics at Pace University, and editor of the Quarterly Journal of Austrian Economics. He has been interviewed in the Austrian Economics Newsletter and on Mises.org. Send him mail. See Joseph T. Salerno’s article archives.

This is a revised version of written testimony submitted to the the Subcommittee on Domestic Monetary Policy and Technology of the Committee on Financial Services, US House of Representatives “Fractional Reserve Banking and Central Banking as Sources of Economic Instability: The Sound Money Alternative,” June 28, 2012.

You can subscribe to future articles by Joseph T. Salerno via this RSS feed.

Copyright © 2012 by the Ludwig von Mises Institute. Permission to reprint in whole or in part is hereby granted, provided full credit is given.